Each year, we work side by side with banks and credit unions that want to update critical systems and refresh traditional business approaches to stay competitive in the digital world. This past year was no different—our clients focused on modernization through technology, and as we reflect on our work in 2022, three things stand out when it comes to using technology effectively for growth:

- Clean, aggregated, real-time data is critical for getting actionable insights and making informed decisions

- Applications should be set up and maintained so they remain scalable and can adapt to changing needs

- Wherever possible, the technology should make users’ jobs easier to accelerate their adoption

Global economic, health, and socio-political headwinds in 2022 drove Financial Institutions to focus even more on digital experiences. They’ve continued to respond to the COVID-fueled mandate for digitization, prioritizing speed, operational resilience, and compliance while keeping an eye on new innovations and industry trends and conditions. And as we look towards 2023, there are further dominoes in motion that will likely play out over the course of the next year:

- Rising interest rates (inflation driven)

- A recession-trending economy

- Geopolitical issues including currency destabilization and economic volatility

- Environmental Social Governance (ESG) Regulations

These issues will likely result in higher borrowing costs, reduced borrowing demand, covenant compliance, collateral values, and default risk. What’s interesting (and perhaps reassuring) is that even though the above pressures are currents that will impact Financial Institutions’ strategies and actions for the next year, the priorities for banks focused on growth don’t change. It still comes down to data, applications, and people. Using these three areas to modernize and optimize banking operations will be key to unlocking greater productivity, stability, and scalability for banks in 2023.

Unlocking Existing Data

In tougher economic times, one of the fastest paths to growth can be using what you already have. While data has always been a critical asset for Financial Institutions, it’s now vital that Banks use their data to better understand their customers and take advantage of emerging opportunities. Unlocking existing data is a cost-effective way to identify and capitalize on growth opportunities during a downward economy—it’s an untapped gold mine of information.

But as we all know, it’s not collecting the data that’s tough—it’s turning data into usable information that’s the real challenge. Exploring and mapping your data can feel like a journey into the wilderness, filled with challenging navigation, changing conditions, and so much more. Banks must have a data strategy and roadmap that guides them to identify, aggregate and analyze their most important data. Through our work, we’ve developed several guidelines to build a strong data strategy:

- Clean data is a critical first step

- Data architecture must be scalable and manageable

- Integrations must be functional and operate in real-time

- Establishing secure data governance is essential

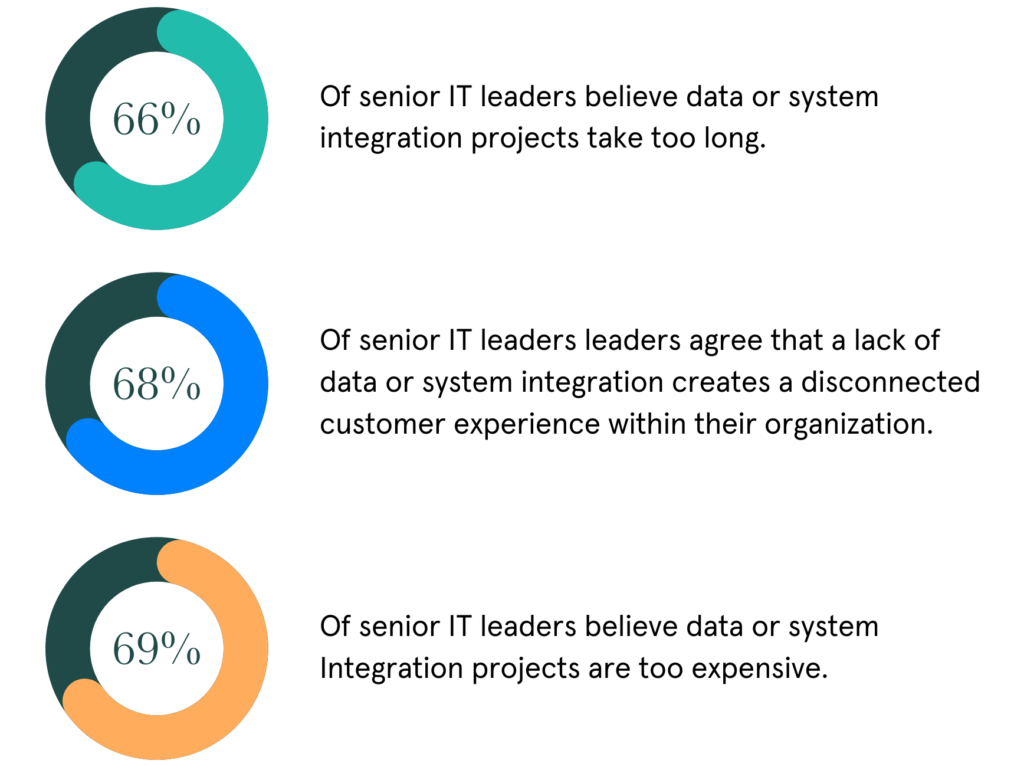

A method that we’ve seen work well for Banks that still struggle with data blockers is starting with a data audit. A low cost diagnostic can often flag risks and highlight opportunities, leading to faster solutions and avoiding long cumbersome projects. And according to MuleSoft IT Leaders Pulse Report, for senior IT leaders, saving time on implementation projects is a top priority.

Using accelerated solutions that pertain to your specific business are also a boon for fast, cost-effective growth during tougher times. Over the last few years of advising Banks, Zennify has developed a banking industry model that standardizes banks’ data across all sources to create a customer Golden Record. Using this model in combination with our data hub has shaved off years of effort for clients.

Using this model in combination with our data hub has shaved off years of effort for clients.

These methods also hedge against the dirty data issue that costs the banking industry trillions of dollars a year (source).

Using Data to Connect

In 2023, consumers’ digital demands will only grow. According to J.D. Power, the biggest influence on customer satisfaction during this period of economic uncertainty is providing a personalized mix of financial advice, hands-on help with problem resolution, and guidance on how to grow their money. If a financial institution provides this level of support, 63% of customers say they definitely will not switch banks, and 78% say they definitely will use their bank for additional services.

A common quandary we see with Banking clients is where to begin using data and analytics, and we see prioritization as a major theme in 2023. With tightened budgets comes a definite need for planning based on business impact. All business units need a full customer view, but the types of data and measurement required are different. So how do you plan data-use projects?

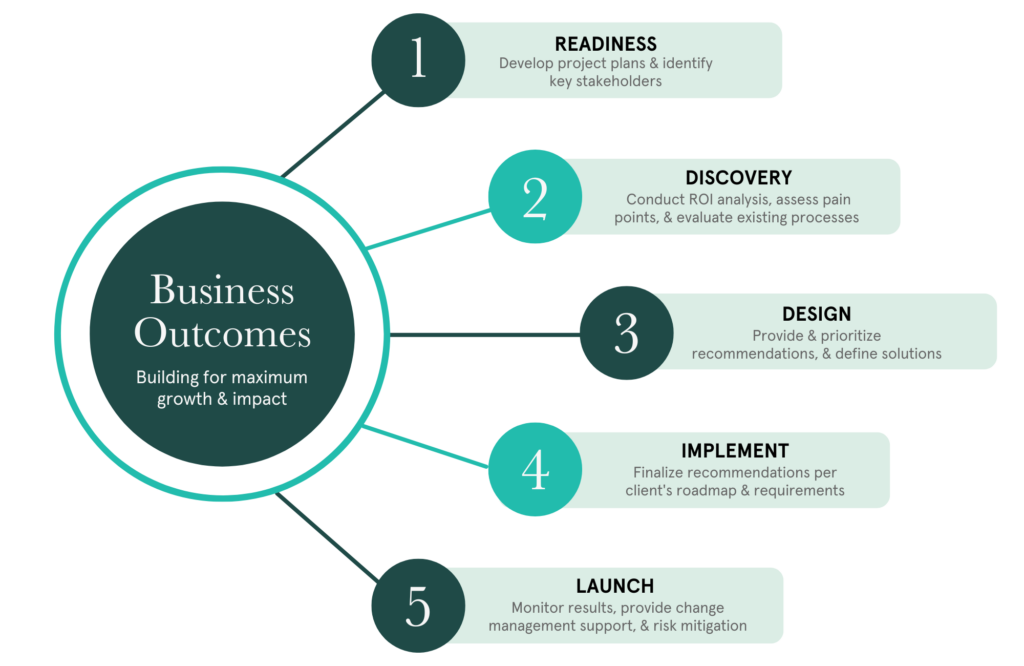

At Zennify, our banking clients have benefited from our Strategic Advisory service that conducts ROI analysis for projects before beginning work. This data is then fed into our banking client’s roadmap, which ensures they are focused on quick wins that drive maximum impact and build on each other to achieve their ultimate business outcomes.

But while we’re focused on data, we always need to remember that this information represents real people with real needs. During challenging times, banking customers want to be treated with care. While proactive help isn’t required, it makes banks stand out and connect with customers on a deeper level. Knowing your customers will help marketing teams deliver smart, helpful product and service recommendations—but delivering that level of personalized service requires readily available, trusted data.

Taking it further, existing banking data can feed machine learning AI algorithms that handle risk-based customer decision making. This can streamline loan and mortgage approvals and processing and free up more time for agents to spend on higher-value client work.

Implementing Cloud Applications

After the 2008 downturn, it was clear that banks needed continuous investment in technology to avoid stagnation and stunted growth. Technology is a critical component for organizations that adapt well and emerge stronger after a recession or global crisis like the COVID-19 pandemic. Reports on business resilience showed that organizations that invested in digital transformation before the pandemic found it easier to pivot and adapt to the challenges (source).

Many larger banks have already adopted cloud-native systems, though it’s rare that any are operating 100% in the cloud. Using an ROI analysis method and identifying the areas where manual tasks, complicated processes, and employee / customer experience are poor is the way to figure out what technology is needed to solve the problem.

Using an ROI analysis method and identifying the areas where manual tasks, complicated processes, and employee / customer experience are poor is the way to figure out what technology is needed to solve the problem.

Cloud-native systems like Salesforce can solve for disparate business challenges, especially when working with a partner who has solved for the same thing before. Pre-existing frameworks and templates make the digitization of business issues well worth the cost. To make applications easy to implement and maintain, look for low-code / no-code implementation. Low-code frameworks can also increase speed to market and are powerful enough to create customer-grade applications without the time, effort, and cost of completely custom builds.

Take digital account opening (DAO), for example. Well-done DAO solutions eliminate a massive amount of keystrokes by pre-filling certain fields from insights already available through primary or secondary data sources. Most importantly, customers should be able to complete a digital account opening process entirely on a mobile device in less than five minutes to reduce drop off. Digital account opening, at the basic level, would have the ability to perform the following:

- Automate basic personal identity information

- Verify applicant identity

- Qualify applicants from a risk/fraud perspective

- Fund digitally in real-time

- Integrate with the core banking system

Cloud applications also enable onboarding new partner channels, which are a great vector for growth in 2023. However, many banks are still struggling to align front- and back-office systems and getting the most out of digital applications also requires ongoing technology platform management. Platforms must be overseen and updated for changing business needs—their adaptability is a primary benefit of cloud-based applications.

With a leaner budget in 2023, it may make sense to partner with outside experts to access the high-skilled resources needed to align, maintain, and grow your platform rather than hiring and training more expensive full-time staff. Zennify’s Managed Services provides clients with a team of technology experts to support their digital transformation needs for a predictable monthly cost that is much lower than aggregate IT expert salaries.

As banks prioritize which lines of business should invest in digital applications, commercial banks in particular should consider Treasury Management. We’ve noticed that these teams are being left behind but need to be on the forefront of digital transformation initiatives as Treasury Services provide essential services for commercial bank customers.

Enabling Your People with Systems & Processes

Optimizing the output of each and every member on a bank’s team will also be a priority in 2023. Assessing each discrete function with an eye towards automating rote, manual tasks that absorb hours is a great place to start. Finding opportunities for automation is critical as operational efficiency is everything during a down economy. Getting on a path to automation isn’t as daunting as it may seem. Again, prioritization is critical. With a sound approach to data, automation comes without too many hurdles.

There also has to be an ongoing focus on employee enablement. Teams must be able to tap into the resources that the Bank already has, including systems, repeatable processes, and more. Systemized, repeatable training can pay off in spades when done well.

When teams have access to tools that make their jobs easier, they have higher job satisfaction, which increases productivity and creates a rewarding cycle resulting in higher margins with happier employees. Change management and training can help employees quickly learn and adopt new processes and technologies to deliver higher ROI faster. Zennify works with clients post-implementation to help accelerate tech adoption through proven change management strategies. Taking the time to light the way forward and give employees a solid foundation to work from will pay both immediate and long-term dividends in terms of productivity and employee engagement.

Plus, just as digital platforms and applications work across teams, departments, and lines of business to support multiple functions and initiatives, executives can benefit from having teams break out of product line structures and organize around the customer experience. Banks that redesign their approach to team collaboration based on high-level business outcomes and performance goals can unlock more innovation.

Defining ESG Policies & Goals

Finally, Banks need to keep up with increasing governmental Environmental, Social, and Governance (ESG) regulations and consumer and stakeholder standards and expectations. Defining and pursuing transparent ESG policies and goals can have a positive impact on multiple levels, from increased stakeholder investment and customer engagement to faster growth (not to mention the positive environmental impact on the world we live in).

However, it can be difficult to gain visibility into supply chains and form partnerships in accordance with stated governance policies. Most businesses are still at the beginning of their ESG journeys, and tackling such a large and important initiative can be overwhelming. But just like other digital transformation projects, start with your data. Technologies like Salesforce NetZero can help you measure where you are now and track your progress towards where you’d like to be in the future.

The Bottom Line: Pursuing Digital Transformation is Key

One thing that’s essential to remember going into the new year is that there’s no magic bullet or panacea for the challenges Financial Institutions will face in 2023. New, flashy innovations like the metaverse or VR will provide distractions rather than solutions. The only sure way to achieve stability and growth is to continue pursuing the pillars of digital transformation: data, applications, and people. This is an ongoing, cumulative effort that may slow down during leaner times, but must still move forward to achieve success.